Daily Habits:

Here are easily implementable, simple and principle based simple DAILY HABITS which build your Financial IQ.

- When you know you are ignorant in a subject, start educating yourself by finding an expert in the field or a book on the subject. All else is thinking without action – the biggest enemy of progress is the idea which keeps you from acting on it.

- Whenever you catch yourself unconsciously comparing your life, worth, wealth to others. Remind yourself, no one has your advantages & disadvantages. You can become a CEO at 30 and die by 35. Similarly, you can build all of your wealth after 50 and live as a most successful investor in the world till 90 like Warren Buffet. The only journey, which you will feel and experience is yours, so make it one which serves others through contribution.

- Realigning the financial spend amount to your real life impact value? Ask yourself twice if I really need it.

- Ask yourself before buying anything that Is this a NEED or a WANT? You might confuse them but they are not the same.

- I am not going to give you your laundry list, as it is your personalised list of don’t wants and wants (Read Part 1). However, I will give you the tools to evaluate when you’re mixing them/confusing them.

- ‘NEED’ equals something which is necessary to sustain life i.e., food, shelter, health, family and living expenses. Everything else is a ‘WANT’ and is negotiable.

Action: Ask yourself every time HOW to get all my WANTS by being smarter and having power and discipline over the NEEDS.

- For example, my friend wanted a Tesla, but it was a WANT. His primary need is to be rich/focus on the asset column and meet his business NEEDS. So he realised the Australian Government was supporting businesses to claim CGT (10% of Sale Price = $80,000 x 10% = AUD$8,000), Luxury tax (~AUD$10,000) and registration support (AUD $3,000 – $5,000) benefit as part of the EV renaissance movement. He leveraged his ‘self-knowledge’ to identify his ‘Want’ & ‘Need’. He then reconsidered his approach using his ‘financial awareness’ and Financial IQ to get his Wants by following Needs.

- A couple who wants to pay for their children’s university, travels and set them up on a strong foundation to be successful can do so by buying a regional investment property, which doesn’t require a hefty mortgage and generates adequate rental income. Looking at the property prices in Australia for past 20 years, I can assure you, you will give them keys to all the WANTS by being intelligent around the NEEDS.

- This isn’t different from RDPD, when Robert’s wife waited for 5 years to get a new Mercedes. She waited till the rental payments offset the car payments essentially meaning there is no increase in risk, commitment or financial burden on life by having a luxury.

- What I respect and deeply admire is the sense of achievement, self belief and knowledge one gets by ‘doing the hard work’ to achieve their values – that is priceless. Alternatively, every new purchase is a 3 week high, on to the next one, to the extent you lose all other core areas of life and become a slave to Rat Race again – being driven by Desire & Fear of not having them.

I do want to caveat, the examples above ONLY work if you have worked the mindset, emotional discipline and have financial awareness around your personal list of DON’T WANTS, which will define the ACTUAL WANTS (Action: Revise PART 1 for more information)

7. Ask yourself at least 3x a day – Am I inventing things to do to AVOID THE IMPORTANT.

8. If you work for money, you give the power to your employer. If money works for you, you keep the power and control it. Some of my favorite, simple things from RDPD:

- The best lesson to me was: “Be smart and you won’t be pushed around as much.” His rich dad was a law-abiding citizen and because it was expensive to not know the law. “If you know you’re right, you’re not afraid of fighting back.” Even if you are taking on Robin Hood and his band of Merry Men.

- Intelligent people are those who work with or hire a person who is more intelligent than they are. When you need advice, make sure you choose your advisor wisely. What I find funny is that so many poor and middle-class people insist on tipping restaurant help 15 to 20 percent, even for bad service, but complain about paying a broker 3 to 7 percent. They enjoy tipping people in the expense column and stiffing people in the asset column. That is not financially intelligent.

9. The way you buy a new dress/suit and think – does it look good in different angles, you check it out from different angles and ask people. Whenever someone says to you it’s only $35 per week, say it to them – that’s a ticket to Istanbul per year. That is $1,820 per year. When someone gives you a figure, take it up and down, twirl in it, ask people if it is the same as my health insurance for the year, think what other mysteries it unlock around your financial freedom.

9. Having a partner (co-pilot) with the same mission as you is a shortcut to financial freedom. We can’t have a millionaire’s wealth strategy with a partner with a minimum wage mindset.

10. Constantly saving without investment is like buying cement to build a skyscraper. When someone asks how life is traveling and you say, I bought cement and I feel good about it. A necessary strategy, but it’s mostly dried up due to cost of living and an expired foundation for a dynamic world with new skyscrapers every few years. See Directions & How to Use to start dreamlining and erecting that high & mighty skyscraper.

11. CONQUERING your fears = DEFINING your fears. You will see the reason most people are able to convert pain into personal success and sacrifice is because they experience your go to quotes like ‘Whatever doesn’t kill you ACTUALLY makes you stronger’ in REAL TIME rather than TikTok/Insta and Social media scroll based experience.

12. Whenever I am roaming around locally in Sydney’s pompous/posh suburbs or traveling abroad, Commonwealth avenue in Boston and Rodeo drive in LA and Madison Square Garden in New York. I love hearing self-serving statements like – It is all inherited money. I usually remind myself and them, WE are INHERITED too. We are also a reflection of inherited values, decision making skills, internal fortitude, financial literacy/IQ and financial survivability. It doesn’t matter what you inherited, what’s important is where you want to be (Read More: Are you Poor, Middle Class or Rich Picture)

Let me emphasise, IT DOESN’T matter which picture accurately reflects you due to personal life circumstances/journey/decisions, what’s important is where do you want to be?

13. Out of all the financial wisdom, advice, literature and get rich quick help I would say that PERSONAL SELF-DISCIPLINE is the MAIN delineating factor between the people who have financial freedom and the ones who don’t.

14. More importantly, the secret to YOUR financial freedom is within YOU!

Directions & How to Use:

- Our beloved government has a whole website and resources available for us to make all our financial dreams a reality – partly since it is funded by taxpayers money. It is called MONEY SMART.

- Also, there there is an amazing Budget Planner Spreadsheet (I know you rolled your eyes, it is ok we all do that to see if there’s a brain there 😛). Jokes apart, it is a great tool to convert your weekly income & expense into monthly, quarterly and yearly estimates. It is so easy and automatic that it is more of a novelty to see things add up and get subtracted.

- Click here to access the ‘spreadsheet’. I know it is such a nerd thing to do and manually reconcile shit – but financially literate adults who have millions are better than rock stars who are homeless. If you do not choose, choice will be made for you. (Quote Wrong/Right).

There are no ‘wrong’ choices in life, just the unconscious ones which dictate the direction & quality of your life and you end up calling it destiny. Everything else comes out in the wash over the long-term as time only moves in one direction – عدنان

- There is an average provided by the Australian Bureau of Statistics around ‘WHAT’S NORMAL BUDGET’ around the country for core needs. The numbers might be a little old, but a good, objective reference point from Government data. Note, these figures are not updated for current YoY highest inflation (Sep 2023: 5.4%, Sep 2015: 1.5%) & interest rates related to housing costs (Sep 2023: 4.10%, Sep 2015: 2.0%) in the past two decades, latest housing prices & TikTok/Insta sales factory.

- A key benefit of Frollo is that it automatically classifies all the historical data under headline (Living & lifestyle) & respective sub-categories. And you can choose what is a ‘NEED’ and a ‘WANT’ for you. For example, I might buy a stroller to give my Godson as a lifestyle/want but for his father is a core need. The classification would be wary for a fair few items every month depending on lifestage and values.

- I joke with people, we should be taxed in accordance with our narcissism. So you write an ego-check every year in line with your worship of hedonism. Primarily, as your personality changes with experience, our spending habits also change in line with our values, life stages and whatever is taking over our attention.

- For example, the electricity bills over the past one year have increased by 20% and if I have a static spreadsheet for a 3-month average spend my cash flow will be blown out everytime I get a new bill.

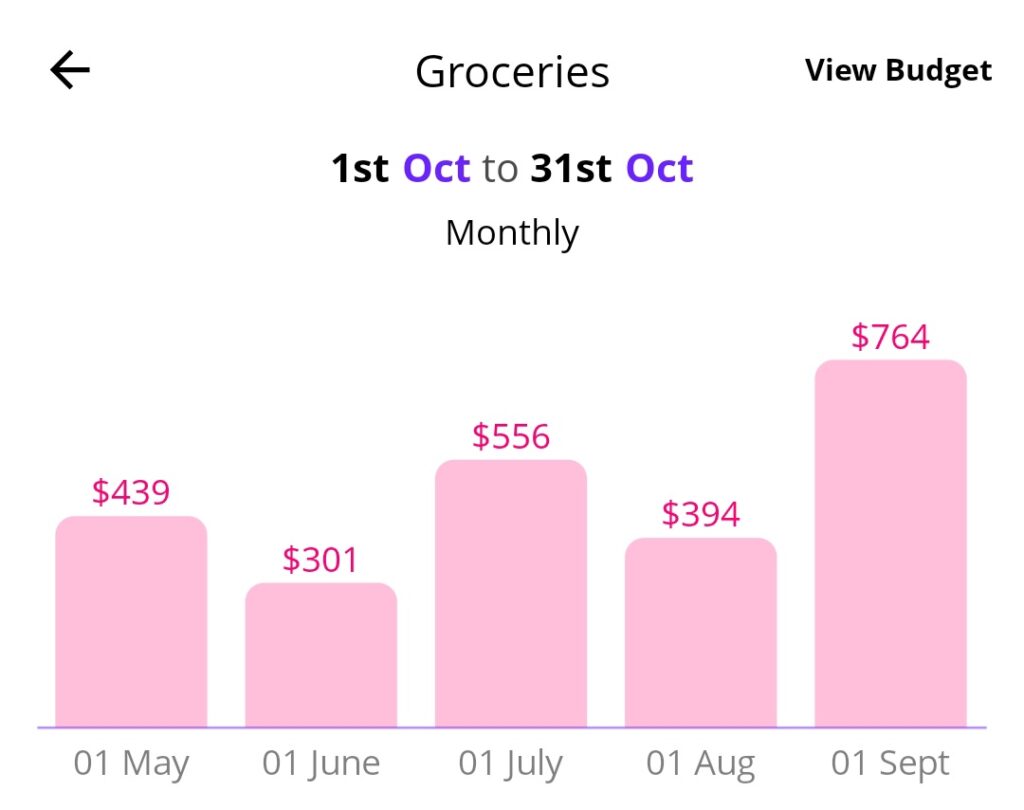

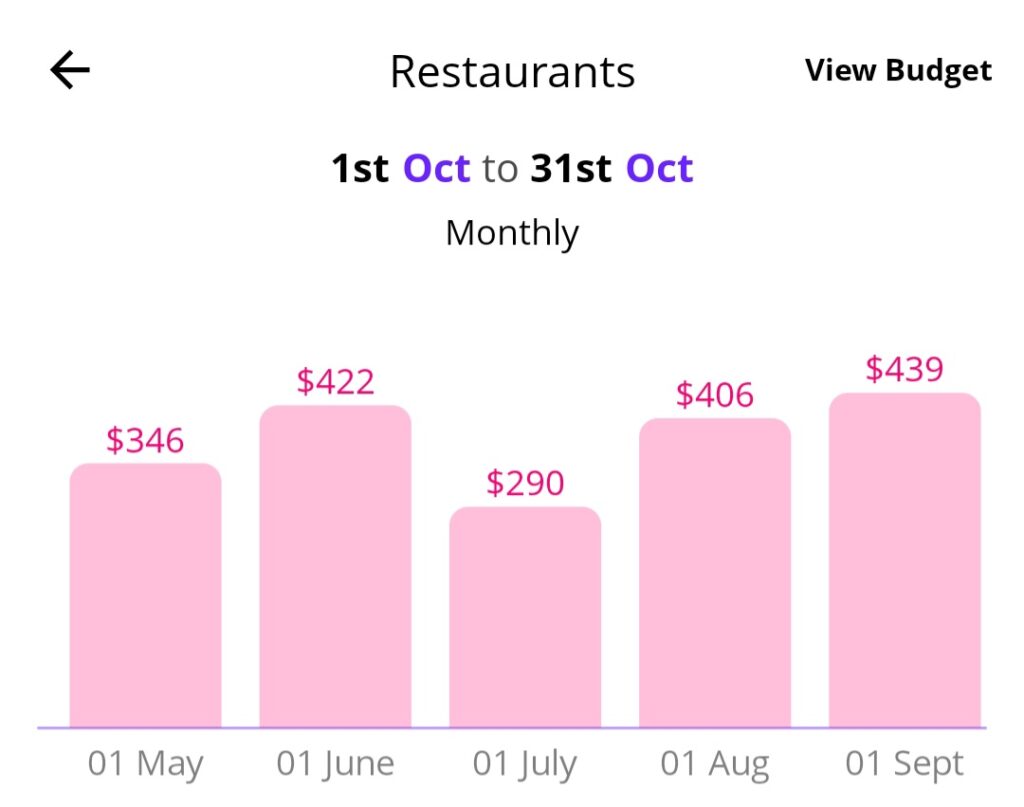

- FROLLO apps tells you that something is changing when compared to the last 3, 6 and 12 months which allows you to preserve/pivot your monthly budget in accordance to dynamic spending habits. Here is an example from my restaurant and groceries spend over the past year – as you can see they vary a lot.

{kind=link}

{kind=link}

This Post Has One Comment

Your writing has a way of making the complex seem simple without losing any of its richness. Each idea is presented in such a way that the reader can’t help but be drawn into it, seeing things from a new perspective. You’ve made something intricate feel effortless, and that’s a true mark of skill.